Cash flow planning is the practice of projecting the money moving into and out of your business so you can fund operations, growth, and obligations without running short. For a growing business, it matters more than profit on paper, because growth consumes cash long before it returns it. A practical cash flow plan combines a forward-looking forecast, a clear view of your timing levers (collections, payments, inventory, and financing), and scenario planning for the decisions on your horizon.

Detweiler Hershey builds this kind of forward-looking cash flow planning into its RAMP Advisory Services, working with growth-oriented businesses across the Delaware Valley and nationally to turn accurate financial records into a plan for what comes next.

Why do growing businesses run into cash flow problems?

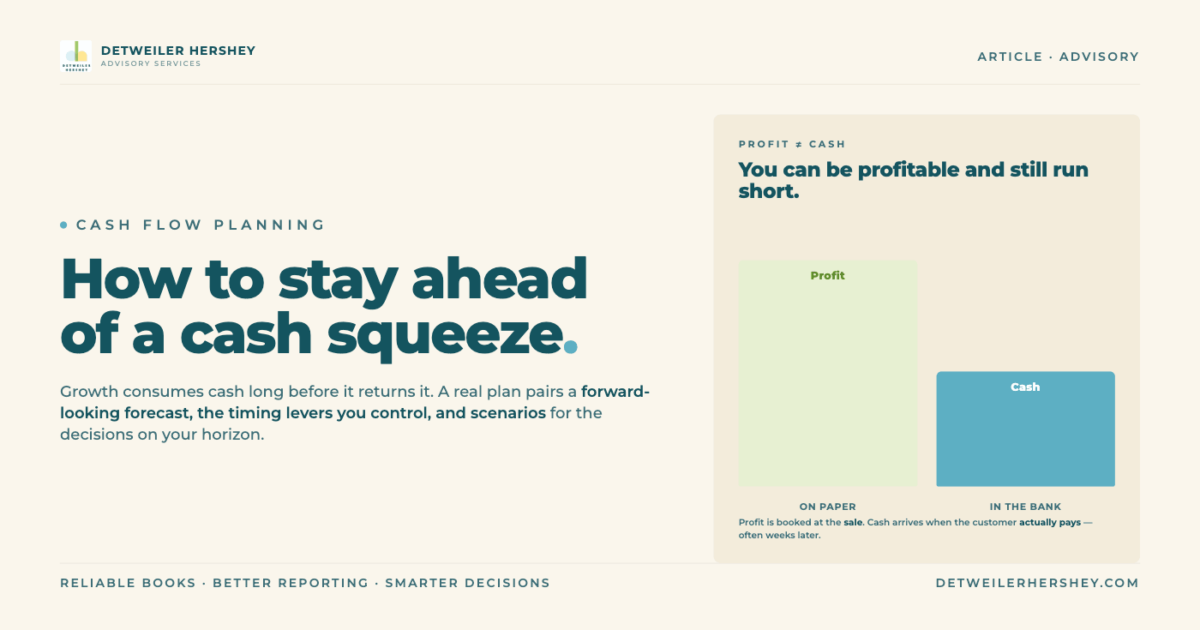

Growth consumes cash. A business can be profitable on its income statement and still run short on cash, because profit and cash flow are not the same thing. Profit is recorded when a sale is made. Cash arrives when the customer actually pays, which can be weeks or months later.

In a growing business, the gap between those two events widens. You hire ahead of revenue, buy inventory before you sell it, and extend credit to customers who pay on their own schedule. Each of those is a normal part of scaling, and each one ties up cash. The faster you grow, the more cash growth demands up front.

This is why fast-growing companies sometimes feel poorer the better they do. The orders are coming in, the business looks healthy, and yet the bank balance keeps tightening. Without a cash flow plan, that squeeze arrives as a surprise, often at the worst possible moment.

What is the difference between profit and cash flow?

Profit measures whether your business is making money over a period. Cash flow measures whether you have money available to spend right now. A business needs both, and the two can move in opposite directions at the same time.

A company can post a strong profit for the quarter while its cash position falls, because customers have not paid yet, inventory is sitting in a warehouse, or a large tax or loan payment is due. The reverse can also happen: a business can have plenty of cash on hand while operating at a loss, simply because it collected on old invoices or took on financing.

For planning purposes, profit tells you whether the business model works. Cash flow tells you whether you can keep the lights on while it works. Growing businesses get into trouble when they watch the first number and ignore the second.

What does a cash flow plan actually include?

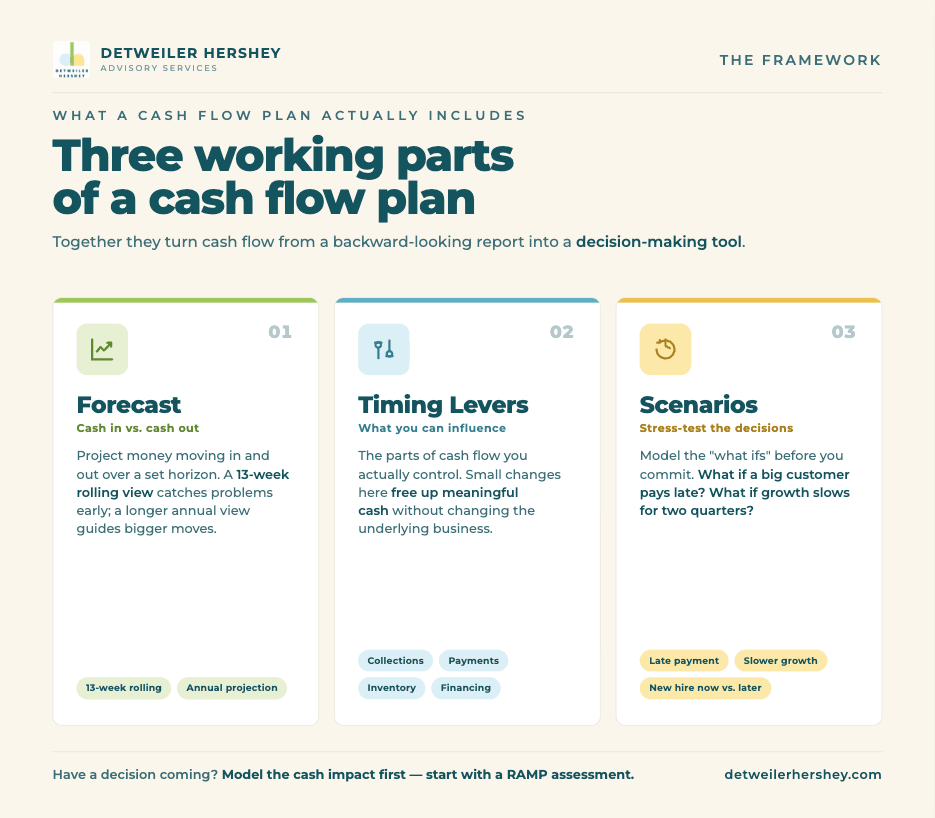

A useful cash flow plan has three working parts: a forecast, a set of timing levers, and scenarios.

The forecast projects cash coming in and going out over a defined horizon. Many growing businesses use a rolling short-term forecast (a thirteen-week view is common) for near-term visibility, paired with a longer annual projection for planning. The short-term view catches problems early. The longer view supports bigger decisions.

The timing levers are the parts of cash flow you can actually influence: how quickly you collect from customers, how you time payments to vendors, how much inventory you carry, and how you use financing. Small changes in these levers can free up meaningful cash without changing the underlying business.

The scenarios test what happens to cash under different conditions. What if a major customer pays thirty days late? What happens to cash if growth slows for two quarters? What if you take on the new hire now versus next quarter? Scenario planning turns cash flow from a backward-looking report into a decision-making tool. For more on two of the core planning tools involved, see Budgets vs. Forecasts: Why Growing Companies Need Both.

How can a growing business improve its cash flow?

Most cash flow improvement comes from tightening timing, not from cutting costs.

On the collections side, invoice promptly, make payment terms clear, follow up on overdue accounts consistently, and consider incentives for early payment. Accounts receivable that sit uncollected are cash you have earned but cannot use.

On the payments side, take the full terms vendors offer without paying late, and align large outflows with periods when cash is strongest. The goal is not to delay paying people. It is to avoid creating an unnecessary cash crunch through poor timing.

Inventory is cash sitting on a shelf. Carrying more than you need ties up money that could fund growth, so matching inventory to real demand frees cash. And financing, used deliberately, can bridge the gap between when you spend to grow and when that growth pays off. Used carelessly, it becomes its own drain. The difference is having a plan.

When should a growing business get help with cash flow planning?

A growing business is usually ready for outside cash flow planning support when the stakes of getting it wrong have risen beyond what an internal bookkeeper or even a controller is equipped to manage. Bookkeeping records what happened. A controller keeps the books accurate and monitors cash. Cash flow planning that looks forward, models scenarios, and informs major decisions is strategic financial work, which is the domain of a CFO.

Detweiler Hershey delivers forward-looking cash flow planning through the CFO/FP&A tier of its RAMP Advisory Services, alongside budgeting and forecasting, scenario modeling, profitability analysis, and strategic support. Cash flow monitoring also features at the Controller tier for businesses that need ongoing oversight before they are ready for full strategic planning. You can see the full scope on the CFO, FP&A, & Controller Services page.

In Detweiler Hershey’s experience, the owners who benefit most are not the ones already in a cash crisis. They are the ones with a real decision coming, a hire, an expansion, a capital raise, who want the cash impact modeled before they commit rather than after. For more on that timing, see When Should You Add Fractional CFO Support to Your Business?

What this looked like for one growing company

When Genzeon, a global technology solutions provider, partnered with Detweiler Hershey, the shift was from reactive accounting to forward-looking financial planning. Monthly financial reviews replaced retrospective bookkeeping with strategy, and reporting that once lived in silos became a single, clear view of the business, including a clearer read on cash.

That forward-looking view is what lets a growing company make decisions with confidence instead of reacting to whatever the bank balance happens to show. You can read the full story in Achieving Financial Clarity and Scalability with Advisory Services.

The starting point for any engagement is a RAMP assessment with the Detweiler Hershey team. Contact us to talk through where your cash flow planning is today and what it needs to become.

Frequently asked questions

How far ahead should a growing business forecast its cash flow?

Use two horizons. A rolling short-term forecast, often around thirteen weeks, gives you near-term visibility to catch problems before they hit. A longer annual or multi-year projection supports bigger decisions like hiring, expansion, or financing. The short-term view keeps you out of trouble week to week, and the longer view keeps you pointed in the right direction.

Can a profitable business still run out of cash?

Yes, and it happens more often than owners expect. Profit is recorded when you make a sale, but cash does not arrive until the customer pays. If you are growing fast, hiring ahead of revenue, carrying inventory, or extending credit, you can be genuinely profitable and still run short on cash. That gap between profit and cash is exactly what cash flow planning is built to manage.

What is the fastest way to free up cash in a growing business?

Usually it is tightening collections. Accounts receivable that sit unpaid are cash you have already earned but cannot use, so invoicing promptly and following up consistently often releases cash quickly. Beyond that, matching inventory to actual demand and timing vendor payments deliberately tend to free up cash without changing the underlying business.

Do I need a CFO to do cash flow planning, or can my bookkeeper handle it?

A bookkeeper records transactions and a controller keeps your accounting accurate and monitors cash, but forward-looking cash flow planning, the kind that models scenarios and informs major decisions, is strategic work that sits with a CFO. A fractional CFO gives you that capability without the cost of a full-time hire. Detweiler Hershey delivers it through the CFO/FP&A tier of RAMP Advisory Services.

How does Detweiler Hershey approach cash flow planning?

Every engagement begins with a RAMP assessment so the work is scoped to where your business actually is. From there, cash flow planning is built on accurate records and reliable reporting, then extended forward with forecasting, scenario modeling, and strategic guidance. The goal is a plan you can act on, not just another report.