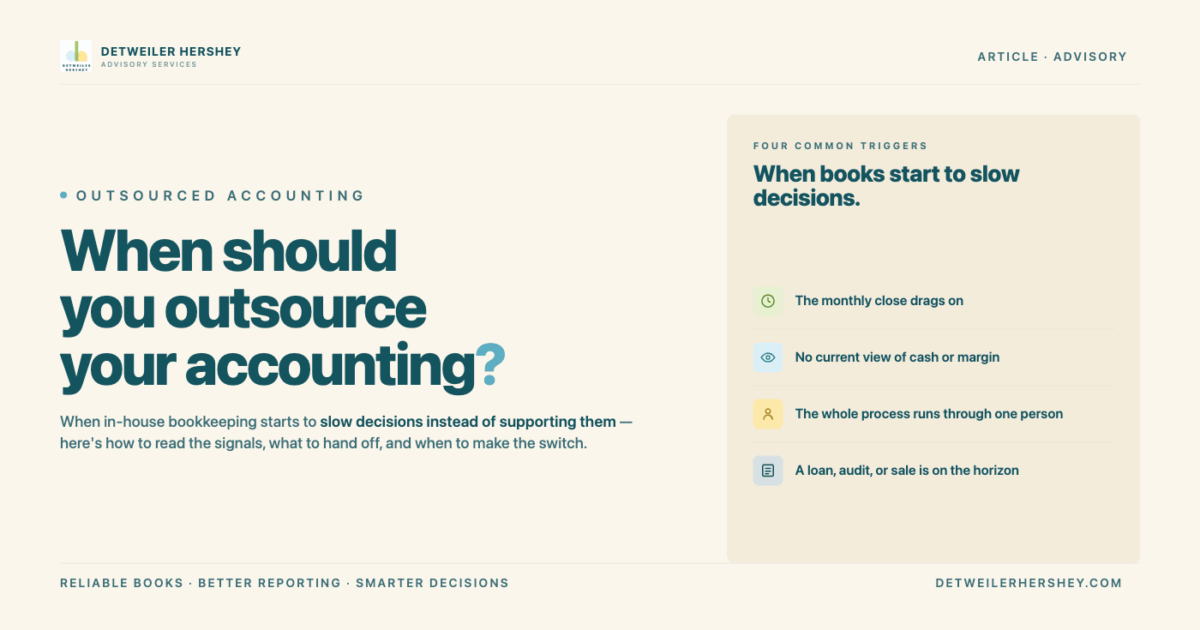

Most growth-oriented businesses should consider outsourcing their accounting when in-house bookkeeping starts to slow decisions instead of supporting them. The common triggers are clear: the monthly close drags past ten business days, leadership has no current view of cash or margin, a bookkeeper leaves and takes the process with them, or a loan, or sale is on the horizon. Detweiler Hershey helps Greater Philadelphia businesses outsource accounting through its RAMP framework, matching each company to the right level of support, from one-time cleanup and monthly bookkeeping up to full fractional CFO leadership.

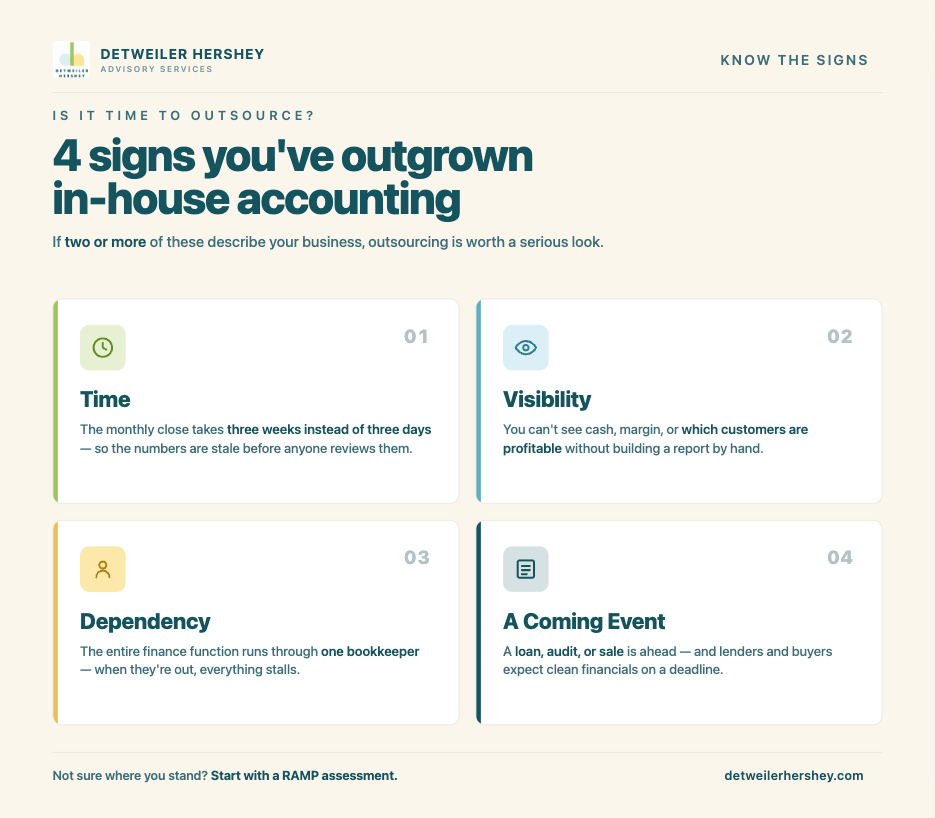

What are the signs your business has outgrown in-house accounting?

The clearest signal is time. When closing the books each month takes three weeks instead of three days, the numbers are already stale by the time anyone reviews them.

A second signal is visibility. If you cannot answer how much cash you have, where margin is trending, or which customers are actually profitable without pulling a report together by hand, your accounting is recording history rather than informing decisions.

A third is dependency on one person. Many small businesses run their entire finance function through a single bookkeeper. When that person is out, on vacation, or resigns, the process stalls and institutional knowledge walks out the door.

A fourth is a coming event. Lenders, buyers, and investors expect clean, organized financials on a deadline. Businesses often discover the state of their books only when a transaction forces the issue, and by then there is little time to fix years of disorganized records.

If two or more of these describe your situation, outsourcing is worth a serious look.

What can you outsource, and what should you keep in-house?

Almost every accounting function can be outsourced. The question is which ones should be.

Transactional work is the easiest to hand off: bookkeeping, reconciliations, accounts payable and receivable, payroll processing, and monthly financial reporting. These are rules-based, time-consuming, and rarely a good use of an owner’s hours.

Analytical and strategic work is where outsourcing adds the most value: budgeting, forecasting, cash flow planning, KPI tracking, and the financial modeling behind big decisions. This is the level most in-house teams cannot staff affordably, because a full-time controller or CFO is expensive and often underused in a smaller company.

What stays with you is ownership of the decisions. Outsourced accounting should give leadership more authority over the numbers, not less. The right partner builds the reporting and analysis; you keep the judgment calls about where the business goes next. For a closer look at two of those analytical tools, see our breakdown of budgets versus forecasts and why growing companies need both.

When is the right time to make the switch?

The right time is before a problem forces your hand, not after.

Outsourcing during a calm period lets a new partner learn your business, clean up what needs cleaning, and build a reliable monthly rhythm without a deadline bearing down.

For many businesses, the practical trigger is revenue. Companies generating between roughly one million and ten million dollars in annual revenue frequently reach the point where DIY bookkeeping no longer fits, but a full-time finance hire is hard to justify. That gap is exactly where outsourced accounting earns its place.

The other natural trigger is transition: a bookkeeper departing, a system migration, rapid growth, or a new ownership structure. Each one opens a window to rebuild the finance function correctly rather than patch it.

How does Detweiler Hershey structure outsourced accounting?

Detweiler Hershey delivers outsourced accounting through RAMP, its proprietary framework built around four steps: Record and Reconcile, Analyze, Measure, and Plan. RAMP is organized into five service tiers so businesses can enter at the level they need today and move up as they grow.

The two entry tiers handle the foundation. RAMP Cleanup is project-based support for businesses with errors, backlogs, or disorganized records. RAMP Foundation is ongoing monthly bookkeeping that keeps records clean, current, and organized: the reliable baseline every higher tier builds on.

The three advisory tiers add insight on top of that foundation. Controller services bring structured financial reporting and transactional oversight. FP&A services add forecasting, budget creation, and cash flow and workforce planning. CFO services deliver long-term strategic planning, benchmarking, and trend analysis. Every engagement starts with a RAMP assessment that matches you to the right tier instead of selling you more than you need.

This tiered design is what separates outsourced accounting from simply offloading data entry. A global technology company that partnered with Detweiler Hershey, for example, moved from reactive bookkeeping to forward-looking financial planning, gaining unified reporting and the accountability to scale. The full story is in the Genzeon case study.

Detweiler Hershey’s position is that outsourcing should never mean handing your finances off blind. Every tier is built to give owners more visibility into their numbers, not less, so the people running the business always understand the story behind the figures.

What does outsourced accounting cost compared to hiring in-house?

Outsourcing almost always costs less than the equivalent in-house team, because you pay for the level of expertise you actually use.

A full-time controller or CFO in the Greater Philadelphia market carries a salary, benefits, payroll taxes, software, and management overhead, often well into six figures before a single report is produced. Many businesses cannot keep a hire at that level busy enough to justify the cost.

Outsourced accounting converts that fixed expense into a scaled one. You access senior fractional CFO, controller, and FP&A expertise for a fraction of a full-time salary, and you add capability only as the business grows. The result is senior-level financial leadership matched to your size, without the cost of building the bench yourself.

For businesses weighing where strategic support fits in, our guide on when to add fractional CFO support walks through the decision in more detail.

Ready to see which RAMP tier fits your business? Start with a RAMP assessment.

Frequently Asked Questions

What does it mean to outsource your accounting? Outsourcing your accounting means hiring an external firm to handle some or all of your finance function instead of staffing it in-house. That can range from monthly bookkeeping and reconciliations to full fractional CFO and FP&A support. You keep ownership of decisions while the firm handles the recording, reporting, and analysis behind them.

Is outsourced accounting only for large companies? No. Outsourced accounting is often most valuable for small and mid-sized businesses, typically those generating between one million and ten million dollars in revenue, that have outgrown DIY bookkeeping but cannot justify a full-time controller or CFO. It gives those companies senior expertise at a size and cost that fits.

Will I lose control of my finances if I outsource? You should not. A well-structured engagement gives leadership more visibility, not less. Detweiler Hershey builds every RAMP tier to put clearer, more current numbers in front of owners so they can make better decisions, while the firm handles the underlying work.

How quickly can outsourced accounting fix messy or backlogged books? It depends on the size of the backlog, but cleanup is usually a defined, project-based engagement with a clear start and finish.

How do I know which level of outsourced accounting I need? The starting point is a RAMP assessment. Detweiler Hershey reviews where your finances stand today and matches you to the right tier, from cleanup and monthly bookkeeping through Controller, FP&A, and CFO services, so you add oversight and strategy only as your business needs it.